Withdrawal order matters most when retirement starts before all income sources are online. A practical sequence should cover the annual gap without creating a larger tax or flexibility problem later.

Why withdrawal order matters

Two retirement plans can have the same total assets and still behave very differently. One can glide through the first ten years with manageable taxes and plenty of flexibility. The other can burn through its easiest dollars too fast and leave only harder tax or timing problems for later.

That is why withdrawal order matters. The question is not only "How much do I have?" It is also "Which dollars should I disturb first, and which dollars are worth protecting for later?"

How bridge years change the answer

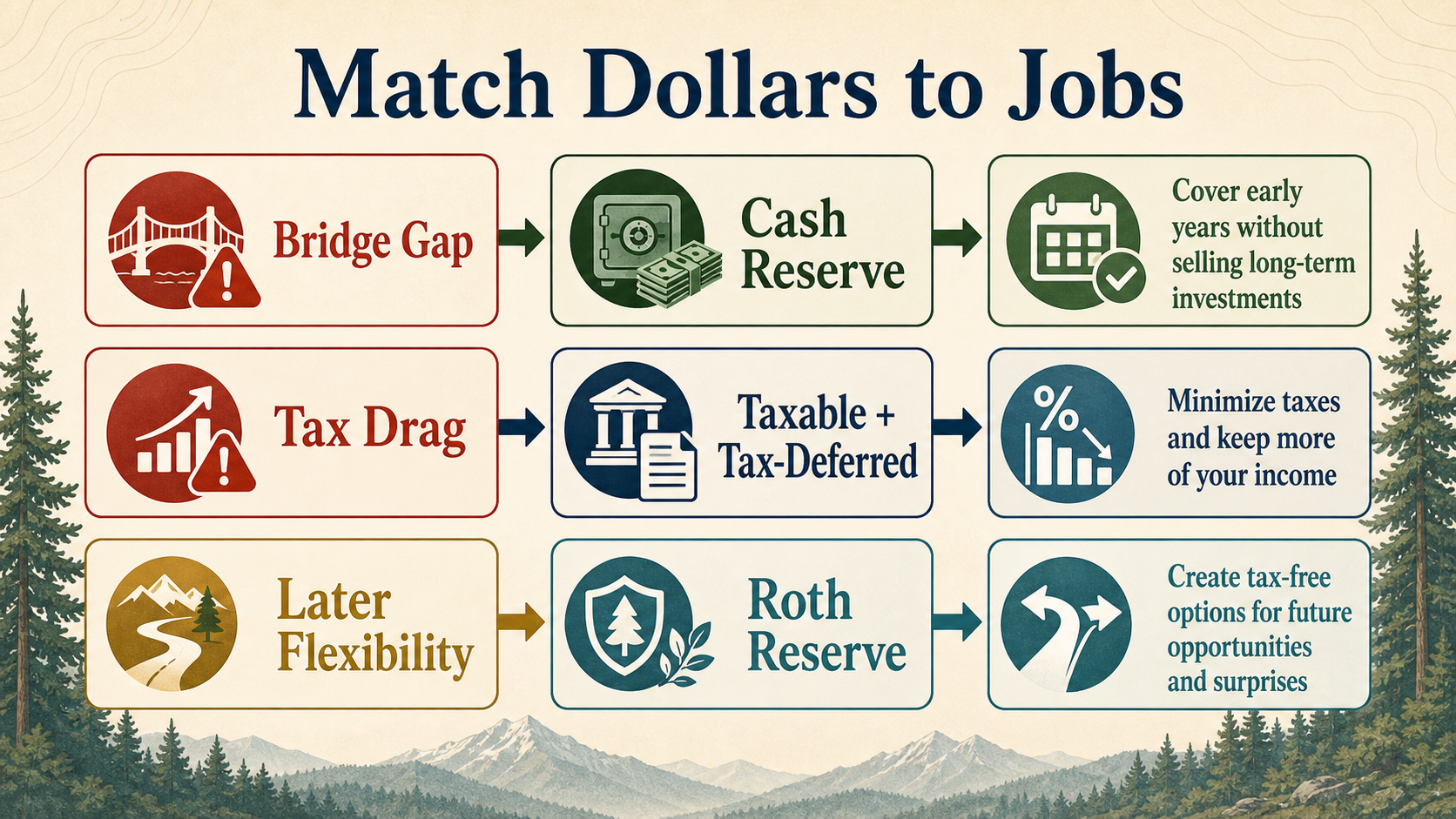

Bridge years are often the hardest years in retirement. That is the stretch after work income ends but before later guaranteed income starts in full. For many plans, that means the years before Social Security begins or before a spouse retires.

During those years, a bad withdrawal order can create pressure in three ways:

- It can force larger taxable withdrawals earlier than necessary.

- It can consume liquid reserves that would have been useful during volatility.

- It can shrink Roth or later-life flexibility before the hardest years arrive.

The best withdrawal order is usually the one that gets you through the bridge years cleanly without creating a worse late-retirement problem.

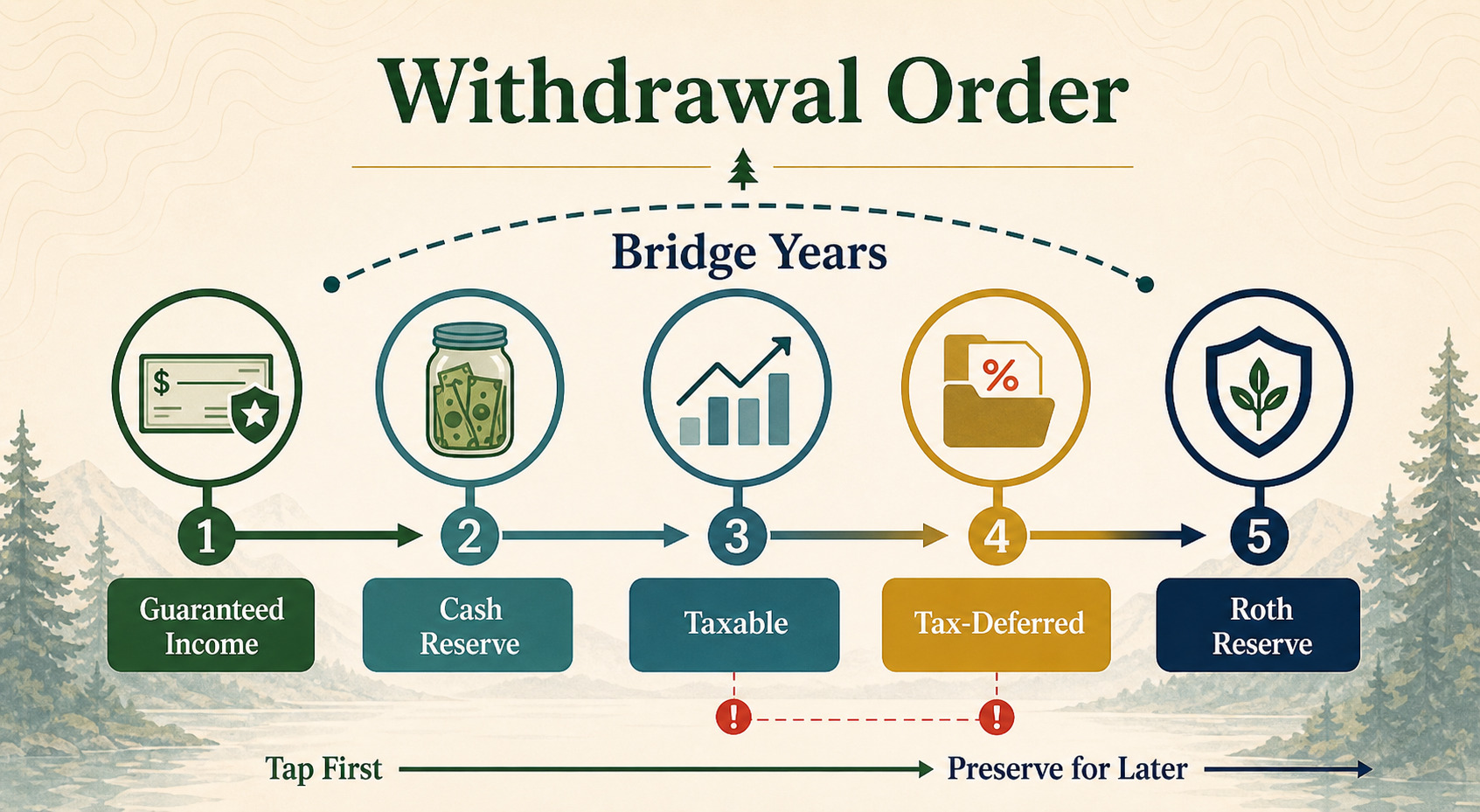

The main account buckets to think about

Most plans involve some mix of liquid cash, tax-deferred accounts, Roth accounts, taxable brokerage, and guaranteed income streams such as pension or Social Security.

Each bucket carries a different job:

- Guaranteed income: the stable base that lowers the size of the spending gap.

- Liquid/cash-like dollars: the cleanest source for short bridge periods and surprise expenses.

- Tax-deferred accounts: often the largest pool, but also the pool that can create tax drag and later RMD pressure.

- Roth dollars: the flexible reserve you usually do not want to waste early unless it solves a real problem.

- Real estate or irregular assets: usually not the first line of withdrawal planning, but still important to the household balance sheet.

A practical planning framework

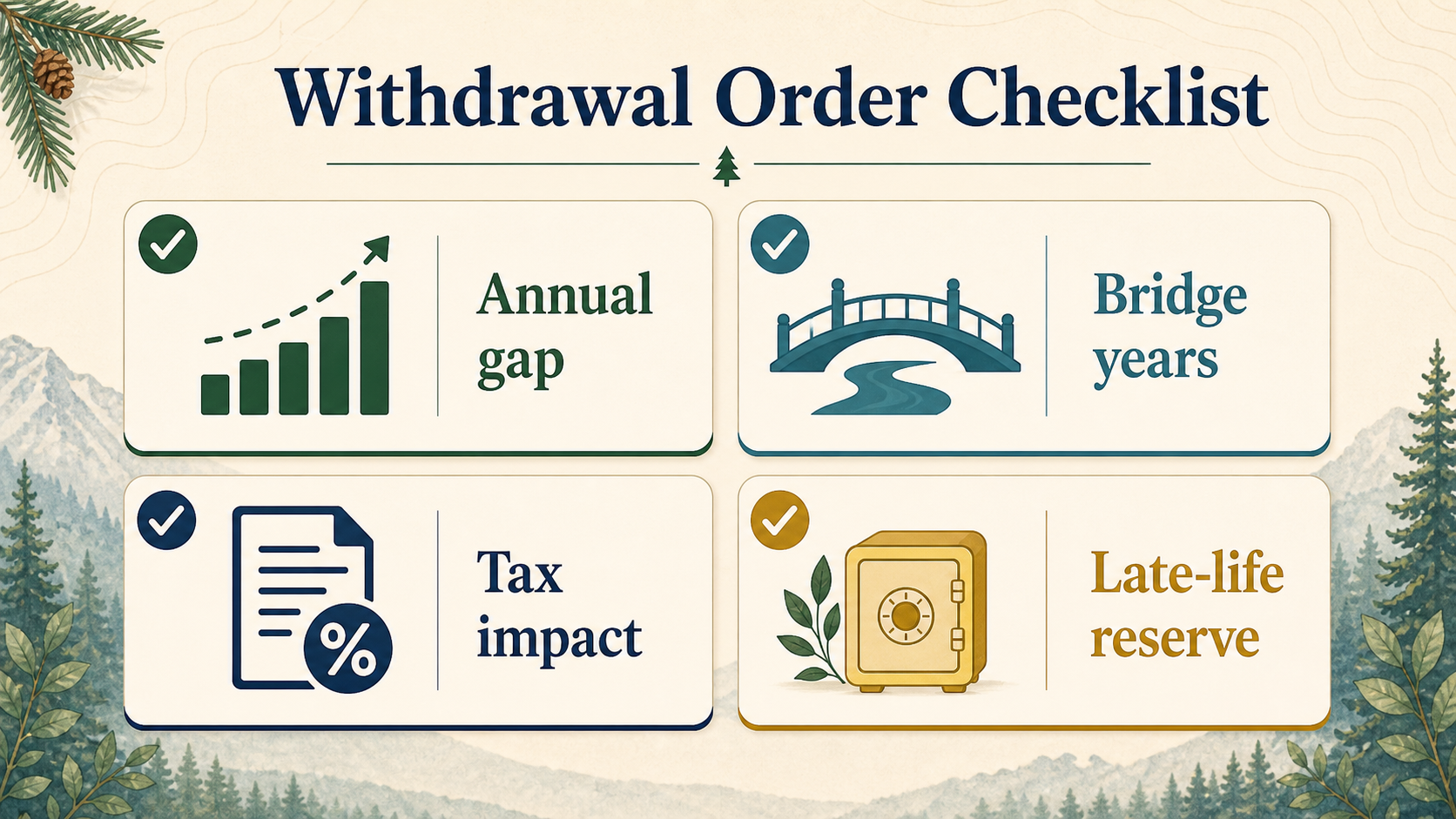

A useful framework is to make the next decision in this order:

- Identify the annual spending gap after pension and any other guaranteed income.

- Measure how many bridge years exist before Social Security or other later income starts.

- Ask which dollars can cover that bridge with the least tax and the least damage to later flexibility.

- Protect Roth and other high-flexibility dollars unless there is a clear reason to use them now.

- Recheck the late-retirement picture so a good bridge choice does not become a bad age-80 choice.

That framework is intentionally simple. It is not tax advice. It is a way to avoid the most common mistake, which is treating every retirement dollar as if it were interchangeable.

When a plan depends heavily on bridge-year withdrawals, tax drag and sequence pressure usually matter more than maximizing every last long-run percentage point.

How LEOFF Helper uses withdrawal guidance

The premium dashboard does not pretend to produce a legally or tax-perfect distribution plan. What it does is organize the current account mix into a more usable planning sequence:

- How many bridge years the plan appears to have

- How large the current bridge gap is

- Which account type looks like the cleanest first bridge source

- How much tax-deferred pressure is building in the background

- Which dollars look worth preserving for later flexibility

That makes the dashboard more useful for a real decision. Instead of showing only assets and success rates, it also starts answering the harder question: "How would we actually fund this retirement path?"

Open the DashboardSources

This guide is primarily a planning-framework article tied to the current LEOFF Helper dashboard behavior rather than a rules summary. For account-specific tax or distribution advice, review the current plan with a CPA or fiduciary professional.