If you retire early, the highest-pressure years may be the years before Medicare and Social Security start. A strong plan needs enough guaranteed income, liquid assets, and expense flexibility to cross that bridge without damaging the rest of retirement.

What is an early retirement bridge?

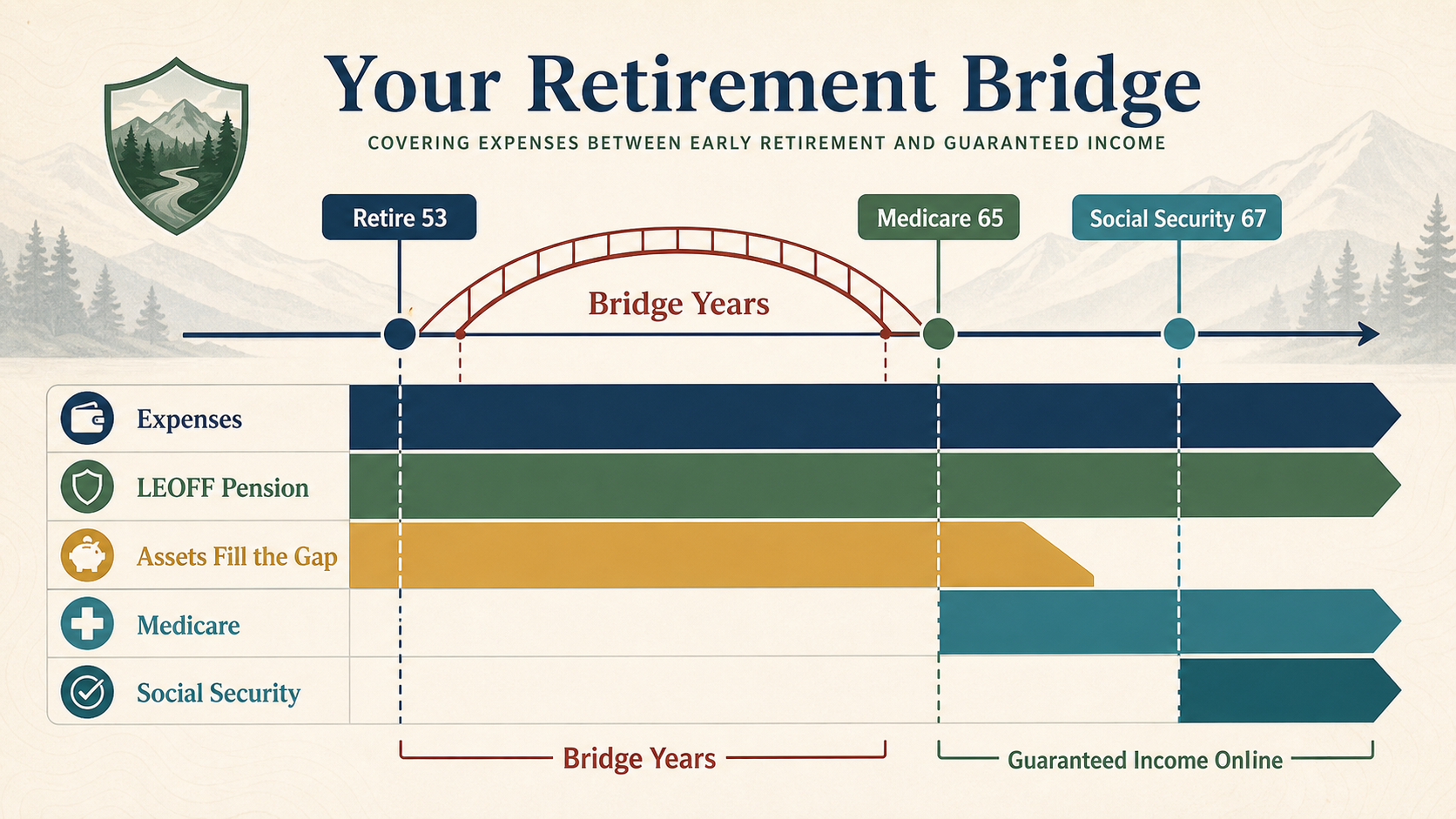

An early retirement bridge is the period between the day you stop working and the day one or more major income sources begin paying.

In practice, bridge years often happen when:

- You retire before claiming Social Security.

- You retire from one system but defer another pension until a later age.

- You want to avoid claiming Social Security too early, so assets need to cover the gap.

- You have recurring expenses immediately, but your full retirement income floor is delayed.

The bridge years are the years when your retirement plan is most exposed to withdrawal pressure.

That is why a plan can look perfectly healthy at age 67 or 70 and still be fragile at age 53, 55, or 60.

If you want to isolate that timing effect first, the Retirement Age Comparison Tool is a useful starting point because it shows bridge years directly for each retirement age before you move into the full simulator.

Pension income may begin, but earned income usually stops or drops.

Savings may need to carry expenses until later benefits begin.

Medicare, deferred pensions, and Social Security can reduce pressure.

Why bridge years are often the weakest part of a plan

Bridge years are risky because they pile several problems into the same window:

- Guaranteed income is lower than it will be later.

- Expenses usually do not wait for Social Security or deferred pensions to begin.

- Withdrawals start earlier, which gives assets less time to compound.

- Early market losses hurt more when withdrawals have already begun.

- Inflation can push bridge costs higher even before the rest of retirement income is fully online.

This is one reason our planning tools do not just ask whether retirement works eventually. They also ask when income becomes strong enough to support the plan without leaning too heavily on savings. You can see that difference in the dashboard through measures like earliest sustainable age, financial freedom, and recommended retirement age.

How Social Security creates a bridge gap

Social Security retirement benefits can start as early as age 62, but SSA says benefits are reduced if you claim before your full retirement age, and they are higher if you wait beyond full retirement age up to age 70.

That means many people face a real tradeoff:

- Claim at 62 and reduce the bridge period, but accept a smaller monthly benefit for life.

- Delay to full retirement age or 70, improve the lifetime benefit, and make the bridge years longer.

SSA pays benefits the month after they are due. If you tell SSA you want benefits to begin in May, your first payment arrives in June. That means cash flow timing matters when you are modeling the first bridge year.

For many LEOFF households, delaying Social Security is mathematically reasonable. But the delay only works well if the bridge is affordable.

How deferred pensions create a second bridge gap

The same problem appears when someone has more than one pension system and does not start them at the same age.

A common Washington example is a LEOFF 2 member who can start a LEOFF pension earlier, but has a vested deferred PERS Plan 2 benefit that does not begin until later. DRS says full retirement for PERS Plan 2 is age 65, though earlier reduced retirement may be available depending on age and service.

That creates a structure like this:

- LEOFF pension starts now.

- PERS benefit starts later.

- Social Security may start later still.

- Assets must carry the difference until all income sources are online.

Washington DRS also notes that members with multiple plans can defer one retirement benefit while receiving another, but you need to work directly with DRS to do that. So this is not a theoretical planning issue. It is a real timing choice in the rules.

What the bridge-year math looks like

The easiest way to see the risk is to compare annual spending with annual income during the gap years.

Example 1: LEOFF starts, Social Security delayed

Assume:

- Retirement at age 53

- LEOFF income: $54,000 per year

- Expenses: $78,000 per year

- Social Security delayed until age 67

Bridge-year shortfall:

$78,000 - $54,000 = $24,000 per year

If that gap lasts 14 years, the plan needs:

$24,000 x 14 = $336,000

That is before factoring in inflation, taxes, or poor early market returns.

Example 2: LEOFF now, PERS later, Social Security later

Assume:

- Retirement at age 53

- LEOFF income: $60,000 per year

- PERS starts at 65 with $12,000 per year

- Social Security starts at 67 with $30,000 per year

- Expenses: $82,000 per year

Ages 53 through 64:

$82,000 - $60,000 = $22,000 annual gap

Ages 65 through 66:

$82,000 - ($60,000 + $12,000) = $10,000 annual gap

Age 67 and later:

$60,000 + $12,000 + $30,000 = $102,000 annual income

After that, income exceeds expenses. But the bridge still consumed:

(12 x $22,000) + (2 x $10,000) = $284,000

Again, that is before inflation or market stress.

Example 3: Why a plan can look fine later and still fail earlier

This is the quiet trap in many plans:

- At age 67, total recurring income may fully cover expenses.

- But from age 53 to 66, the household may be drawing heavily from savings every year.

- If assets fall early, or inflation is higher than expected, the plan can weaken before the stronger income years ever arrive.

That is why bridge-year analysis matters. The question is not only whether the later retirement years look good. The question is whether the plan can safely reach those years.

What makes a bridge stronger?

Bridge years become safer when one or more of these is true:

- Your guaranteed income already covers essential expenses.

- You have enough liquid assets to fund the gap without stressing the rest of the plan.

- You retire a little later, shrinking the bridge.

- You reduce fixed expenses before retiring.

- You phase work income down instead of stopping all earnings at once.

Many households do not actually need the bridge to cover all spending. They need it to cover essential spending. That distinction matters. A flexible lifestyle budget is easier to bridge than a fixed-cost household.

What to test before you retire early

- What is your annual gap before Social Security begins?

- If you have another pension, when does that pension really start?

- How many years must assets cover expenses before all recurring income is online?

- Would the bridge still work if inflation is higher than expected?

- Would the bridge still work if markets are weak right after retirement?

These are exactly the kinds of issues you can test in the calculator and review through the dashboard timeline and vulnerability analysis.

Bottom line

The bridge years are easy to overlook because they often disappear once you look far enough out in the projection. But they can still be the most fragile part of the plan.

If you retire before Social Security starts, or before a deferred pension starts, the real question is not just whether retirement works eventually. It is whether your plan can safely cross the bridge.

Test Your Bridge Years in the CalculatorSources

Social Security Administration, You Can Receive Benefits Before Your Full Retirement Age. Used for SSA's rule that retirement benefits can start as early as age 62, that claiming before full retirement age reduces the benefit, and that payments are made the month after they are due.

Social Security Administration, Delayed Retirement Credits. Used for the rule that delaying beyond full retirement age increases retirement benefits, with no additional increase after age 70.

Washington State Department of Retirement Systems, LEOFF Plan 2. Used for LEOFF 2 full retirement at age 53 and early-retirement context.

Washington State Department of Retirement Systems, PERS Plan 2. Used for PERS Plan 2 full retirement at age 65 and reduced early-retirement availability.

Washington State Department of Retirement Systems, Multiple Plans. Used for DRS guidance that one retirement benefit can be deferred while another is received.