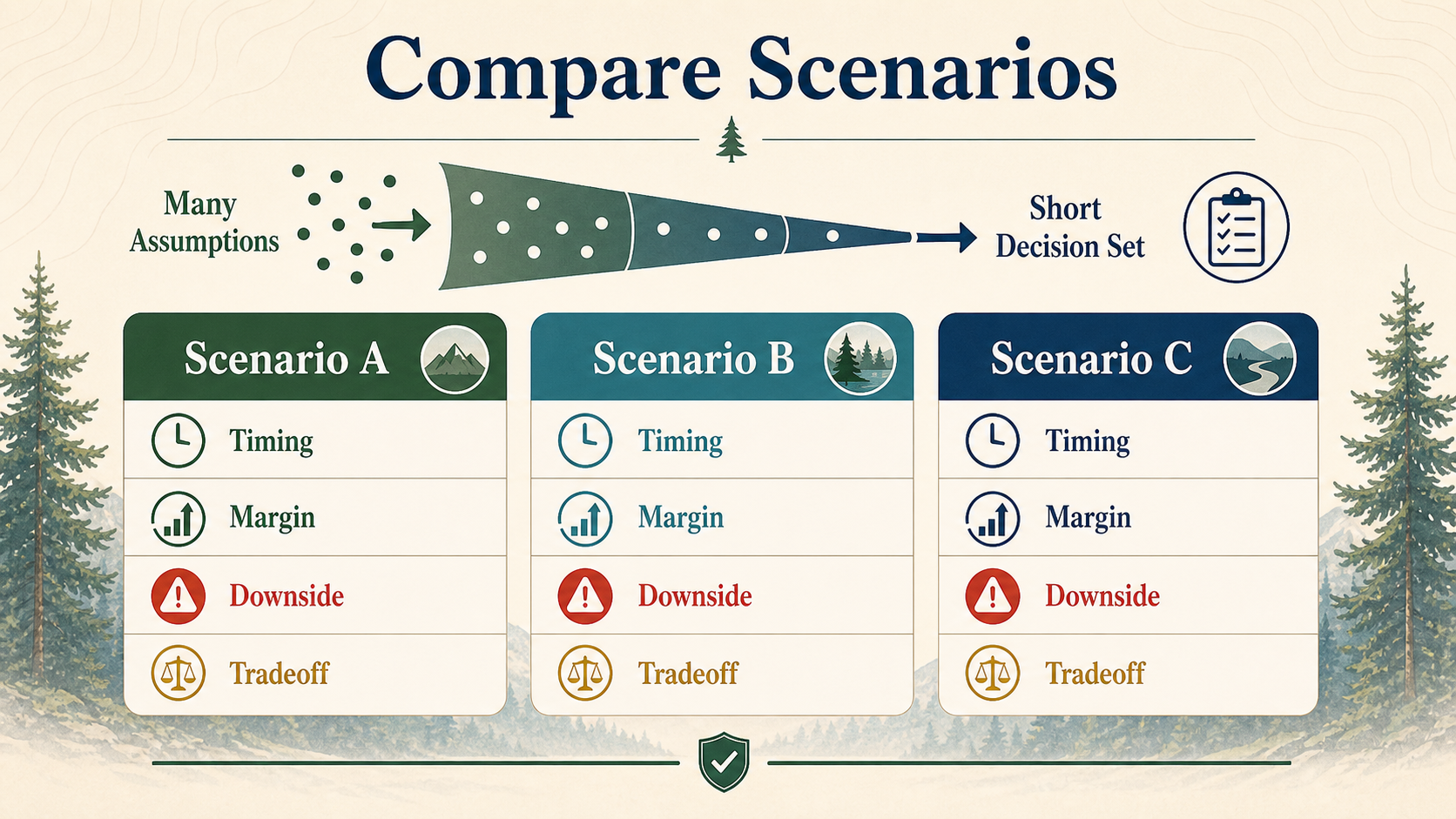

A useful comparison starts with two or three decision-shaped scenarios, then checks timing, margin, downside durability, and tradeoff cost before adding more detail.

Why scenario comparisons get messy

Many people compare retirement scenarios by changing a dozen assumptions at once. Then the comparison becomes impossible to read because no one can tell which change actually caused the better or worse result.

Good scenario comparison is narrower than that. It is not about producing the largest table. It is about isolating the choices that matter enough to affect timing, household resilience, or downside risk.

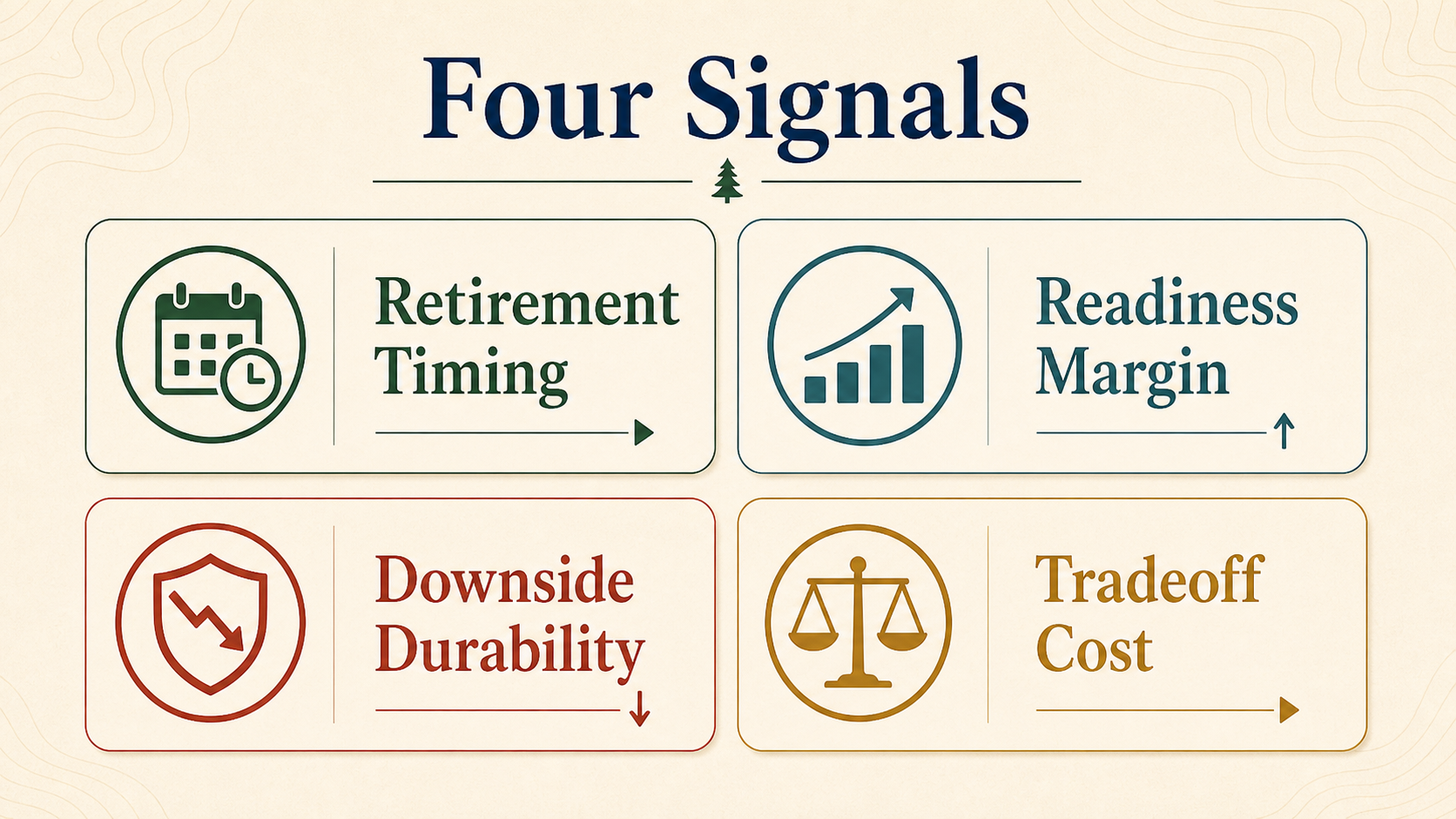

The four signals worth comparing first

A practical first-pass comparison usually only needs four signals:

- Retirement timing: what age the scenario assumes and whether that timing still looks justified.

- Readiness or margin: how comfortably income covers expenses at retirement.

- Downside durability: when deficits or depletion appear if the plan is pressured.

- Tradeoff cost: what you gave up to get the stronger result, such as extra work years or lower flexibility.

A useful scenario comparison does not ask which plan looks best in isolation. It asks which tradeoff is most worth making.

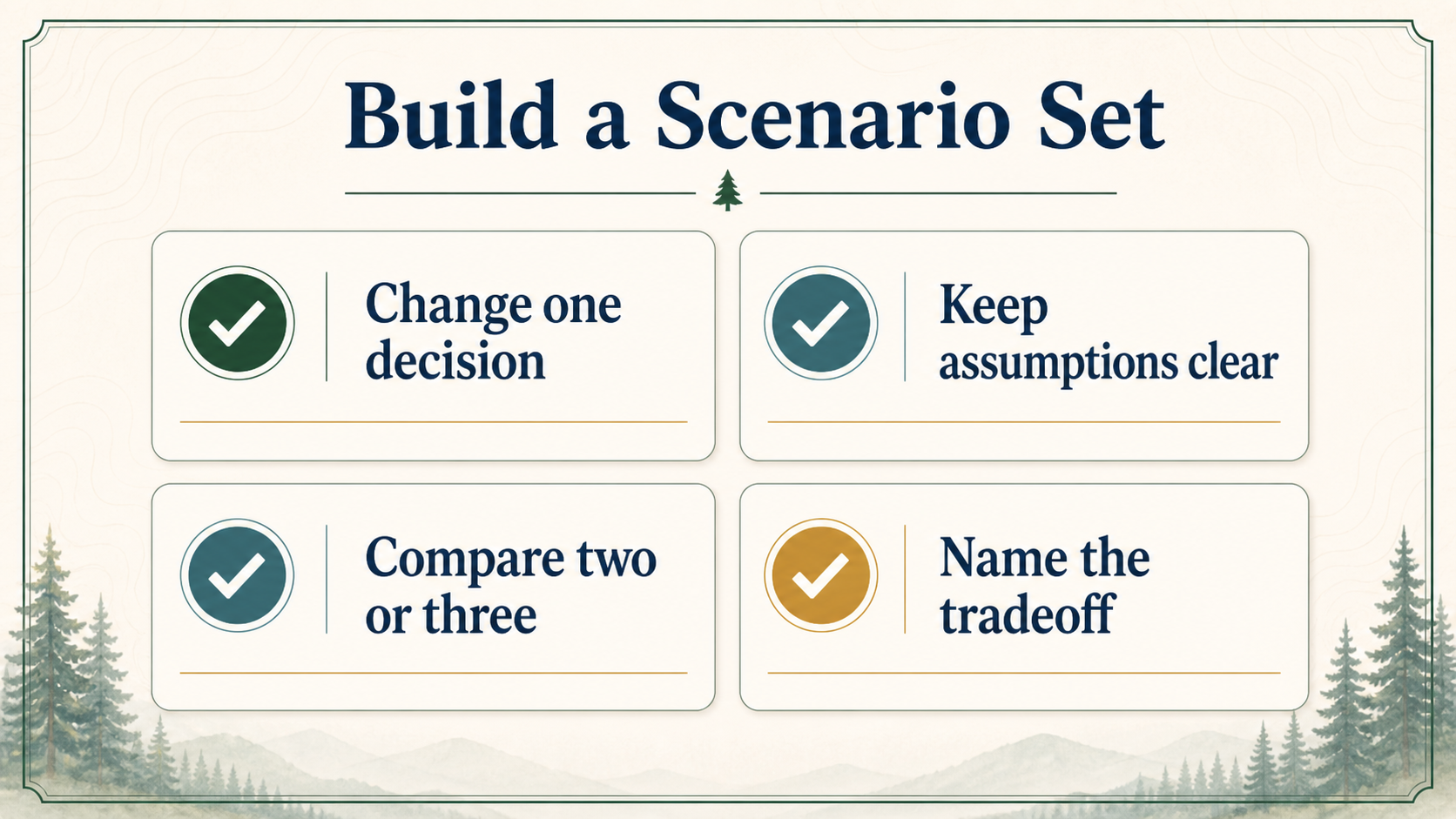

How to build a good scenario set

The cleanest scenario sets usually change one real-life decision at a time. For example:

- Retire at 53 versus 55

- Claim Social Security earlier versus later

- Pay off the mortgage before retirement versus carry it

- Keep the survivor election versus reduce it

- Hold one more year of bridge cash versus invest more aggressively

That produces scenarios that are decision-shaped instead of spreadsheet-shaped. You can explain them to a spouse, and you can act on them.

Do not compare eight scenarios at once unless they are already filtered down to the few that represent real candidate decisions.

What a useful scoreboard looks like

A good scoreboard does not need every field. It needs enough structure to show which scenario leads on the important points:

- Which one has the strongest readiness or retirement-year margin

- Which one survives stress better

- Which one preserves more optionality

- Which one requires the biggest lifestyle concession

If you cannot describe the winner and the cost of winning in two or three sentences, the comparison probably needs to be simplified.

How LEOFF Helper supports scenario comparison

LEOFF Helper already supports saved scenarios, and premium comparison adds more detail around readiness, retirement-year margin, depletion timing, and other decision cues. The point is not to create more complexity. The point is to make it easier to compare real retirement choices without losing the story.

That is also why the dashboard now includes simpler packet layers. Sometimes a decision needs a full report. Sometimes it needs a brief that tells a spouse or advisor what changed, why it matters, and what tradeoff is actually being made.

Open the CalculatorSources

This guide is based on the current LEOFF Helper scenario-management and dashboard-comparison workflow rather than a single outside rules source. It is meant to provide a cleaner decision framework for using the existing planning tools.