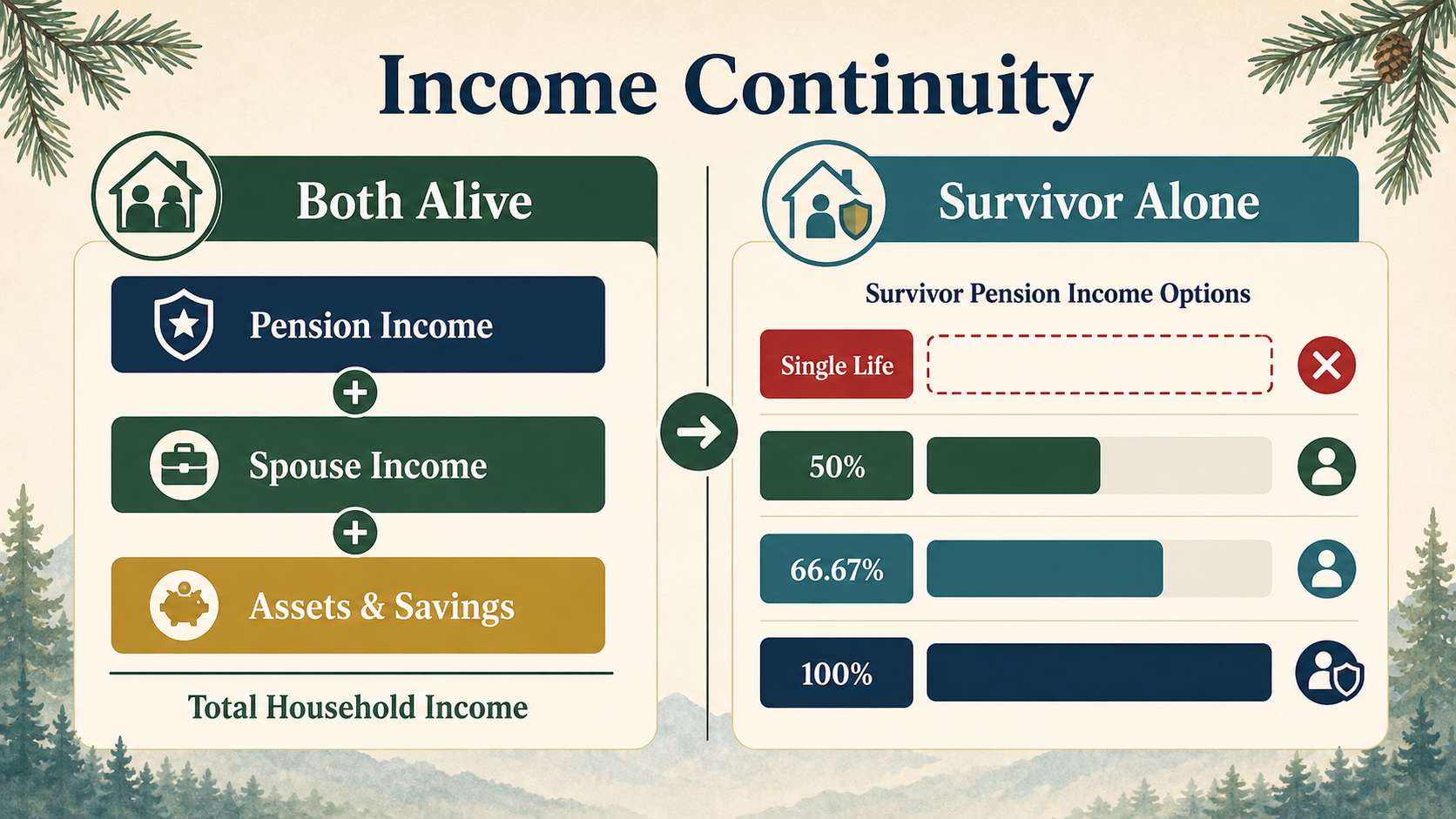

A survivor election is a household income decision. Compare what the pension pays while both spouses are alive against what the surviving spouse would keep if the retiree dies first.

What survivor options does DRS offer?

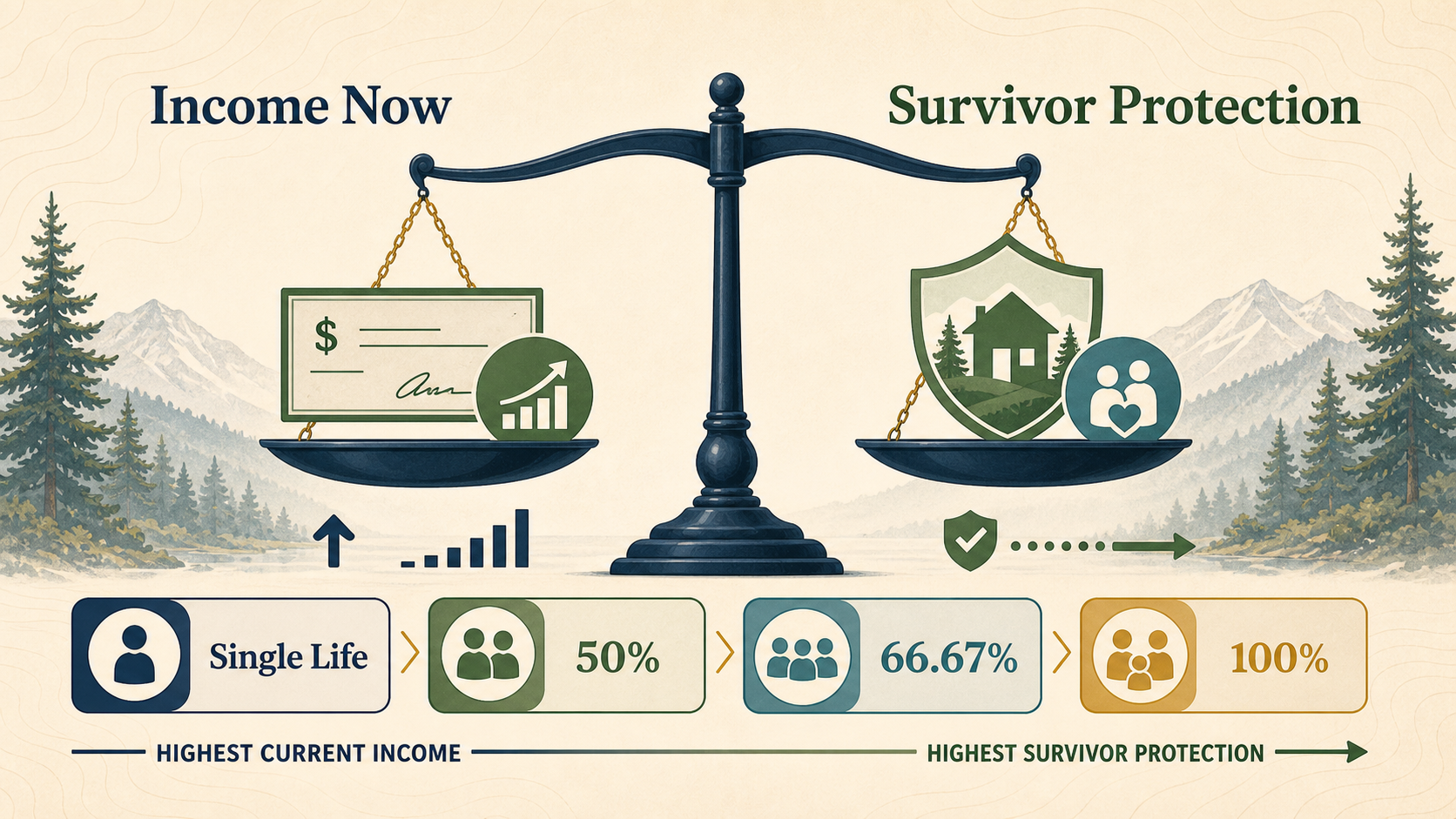

Washington DRS says that when you retire, you choose one of four main benefit options:

- Option 1: Single life. Pays the highest monthly benefit to you, but the pension ends when you die.

- Option 2: Joint and 100% survivor. Pays you a reduced monthly benefit, and your survivor gets that same monthly amount for life after your death.

- Option 3: Joint and 50% survivor. Pays you more than Option 2, but your survivor gets half of your monthly amount for life.

- Option 4: Joint and 66.67% survivor. Sits between the 100% and 50% options.

DRS also makes two other important points:

- You can name only one survivor per retirement plan, and the choice is generally permanent.

- If you choose single life, or if you name someone other than your spouse or registered domestic partner, DRS requires notarized spouse or partner consent.

The survivor election is really a trade: more income while both spouses are alive now, or more income protection for the surviving spouse later.

The real tradeoff is household income, not just pension income

Many people look at survivor options only as a pension reduction question: "How much monthly income am I giving up now?" That matters, but it is not the whole decision.

The better household question is:

If one spouse dies first, how much income does the household still keep?

That answer depends on more than just the pension. It also depends on:

- whether Social Security changes for the surviving spouse,

- whether expenses fall only slightly or by a meaningful amount,

- whether the household still has mortgage or debt obligations, and

- how much of retirement security depends on stable monthly income rather than assets.

This is why survivor planning belongs inside the bigger retirement plan. In your calculator and retirement dashboard, the right question is not just which option pays you the most while you are alive. It is which option leaves the household resilient after a loss.

If retirement timing is still your first question, start with the Retirement Age Comparison Tool and then layer survivor choices into the full calculator once you know which ages you want to test more deeply.

A clean 10-year survivor-income example

Washington DRS provides a simple example for a monthly pension of $2,122, with the member and survivor within five years of the same age:

- Single life: $2,122 per month to the retiree

- 100% survivor: $1,763 per month to the retiree, then $1,763 per month to the survivor

- 50% survivor: $1,926 per month to the retiree, then $963 per month to the survivor

- 66.67% survivor: $1,869 per month to the retiree, then $1,233 per month to the survivor

If the survivor lives 10 more years after the retiree dies, the pension income paid to the survivor would be:

- Single life: $0

- 100% survivor: $1,763 x 12 x 10 = $211,560

- 50% survivor: $963 x 12 x 10 = $115,560

- 66.67% survivor: $1,233 x 12 x 10 = $147,960

That example makes the tradeoff much easier to see:

- Single life pays the most to the retiree now, but provides no continuing pension income to the spouse after death.

- 100% survivor gives up the most now, but preserves the most household pension income later.

- 50% survivor protects the least after death, but reduces the retiree's monthly benefit the least among the joint options.

- 66.67% survivor often lands in the middle as a compromise option.

These are DRS example numbers, not universal formulas. Your actual reduced benefit depends on the ages of both the member and survivor. DRS publishes survivor option factor tables for LEOFF members because age difference changes the reduction.

If you want to compare that tradeoff with your own service years, salary, and spouse age, use the Survivor Benefit Estimator. It is designed to make the range of outcomes easier to see without pretending to predict mortality.

Why age difference matters

DRS publishes survivor option factors for LEOFF members that vary depending on whether the member is older or younger than the beneficiary and by how many years. That means the same survivor option can reduce the retiree's monthly benefit differently depending on the couple's ages.

In general, the larger the expected survivor-payment commitment, the larger the reduction tends to be. So if your spouse is meaningfully younger than you, the cost of choosing a high survivor percentage can be larger than it looks in a same-age example.

When each option may fit best

Single life may fit when

- the spouse has their own strong pension or income floor,

- the household has substantial assets,

- the spouse would not depend heavily on the pension after your death, or

- you are prioritizing the highest current monthly income and have fully accepted the survivor tradeoff.

100% survivor may fit when

- the spouse depends heavily on your pension income,

- the household wants the strongest income continuity after a death,

- the surviving spouse would struggle with a large drop in monthly income, or

- you want the cleanest household-income handoff.

50% or 66.67% survivor may fit when

- the spouse has some income of their own but not enough to fully replace the pension,

- you want more income now than the 100% option provides, but still want meaningful survivor protection, or

- you are trying to balance resilience with current affordability.

This is also where other retirement choices matter. For example, if you are also thinking through tiered multiplier vs lump sum, the stronger monthly pension path can sometimes make a survivor option easier to absorb because the starting monthly benefit is higher before the reduction.

What happens if your survivor dies before you?

DRS says that after you retire, if your survivor dies before you, you can contact DRS to have your benefit changed to the unreduced single-life amount. That matters because it means the survivor reduction is not necessarily locked in forever if the survivor predeceases you.

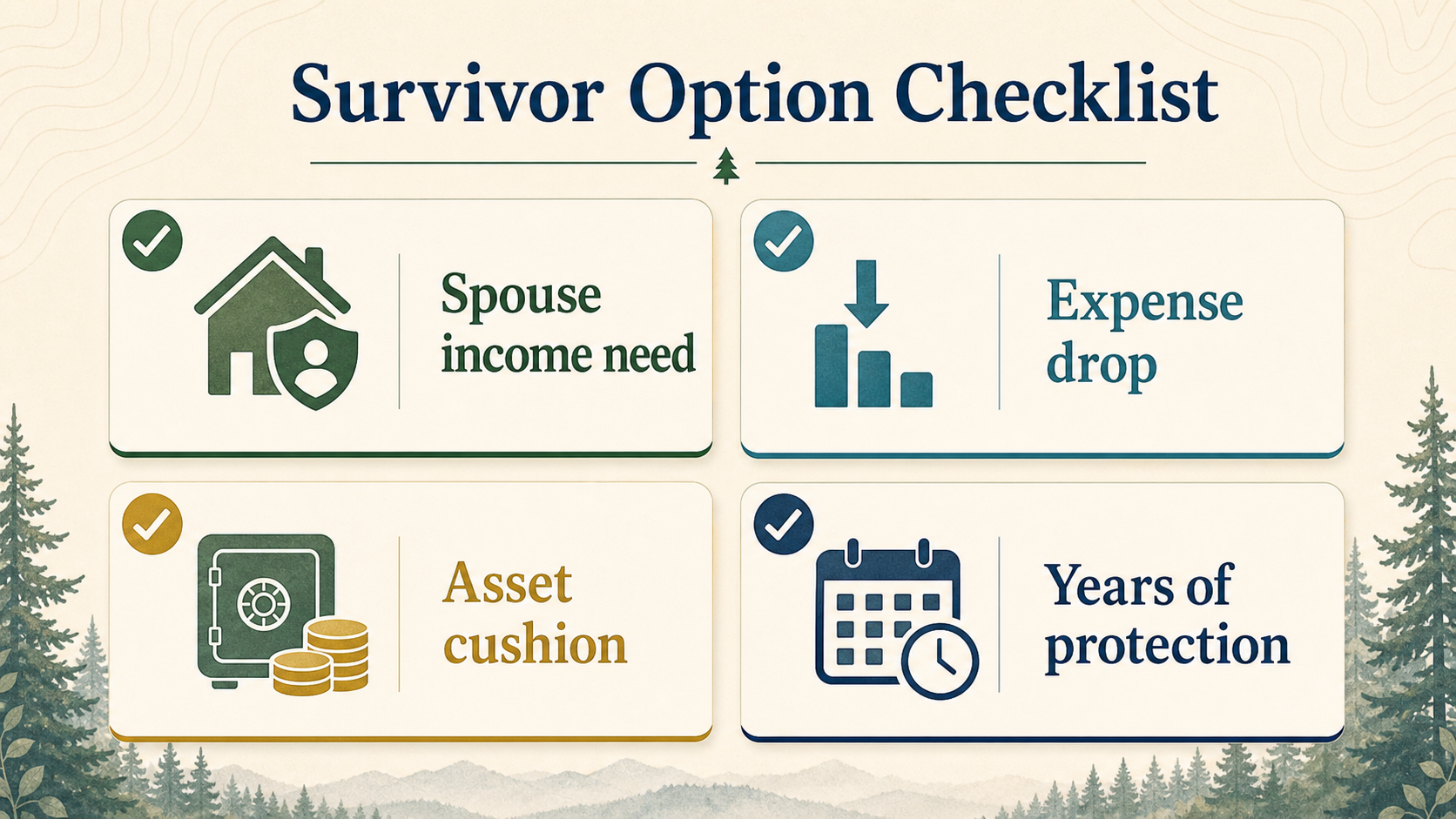

What to test in your retirement plan

- How much monthly income does the household lose at the first death under each survivor option?

- Would the surviving spouse still have enough recurring income to cover essential expenses?

- How much does each option reduce retirement income while both of you are alive?

- Is the household relying on assets to fill the post-death gap?

- Would the survivor option still feel right if one spouse lives another 10, 15, or 20 years?

These are exactly the kinds of comparisons that become more meaningful when you also think about bridge years and market vulnerability. A spouse who loses pension income during a weak market environment may need a stronger income floor than the base-case plan suggests.

Bottom line

Survivor elections are one of the clearest examples of a retirement decision that should be made at the household level, not just the individual level.

The best option is not always the one with the highest current monthly benefit. It is the one that leaves the household most resilient after a loss, given your spouse's income, your assets, your expenses, and how long the surviving spouse may still need the income.

Open Survivor Benefit EstimatorSources

Washington State Department of Retirement Systems, LEOFF Plan 2. Used for the survivor-option descriptions, DRS's example monthly pension amounts under the four retirement options, spouse or domestic partner consent rules, and the rule that a retiree can request restoration to the single-life amount if the survivor dies first.

Washington State Department of Retirement Systems, Survivor benefit option factors for LEOFF members. Used to support the point that survivor reductions vary by the ages of the member and beneficiary.