Start with the plan you can model yourself. Bring in a CPA, fiduciary financial professional, or both when taxes, liquid assets, timing decisions, or household complexity make the cost of a mistake too large.

When do-it-yourself planning starts to break down

There is nothing wrong with managing your own finances when life is still simple. Many households can handle budgeting, saving, retirement contributions, and even basic investing without paying a professional.

But the breaking point often arrives quietly. It is usually not one big event. It is a pileup of more important decisions:

- larger taxable accounts,

- retirement timing questions,

- Social Security coordination,

- asset-location and tax issues,

- inheritance or estate questions, and

- mistakes that now carry real dollar consequences.

The right time to seek professional help is often the point where a 10% mistake would have consequences you do not want to absorb on your own.

That is especially true as retirement gets closer. A household with strong income and many working years ahead can recover from errors more easily than a household approaching retirement with a large portfolio and fewer years to fix them.

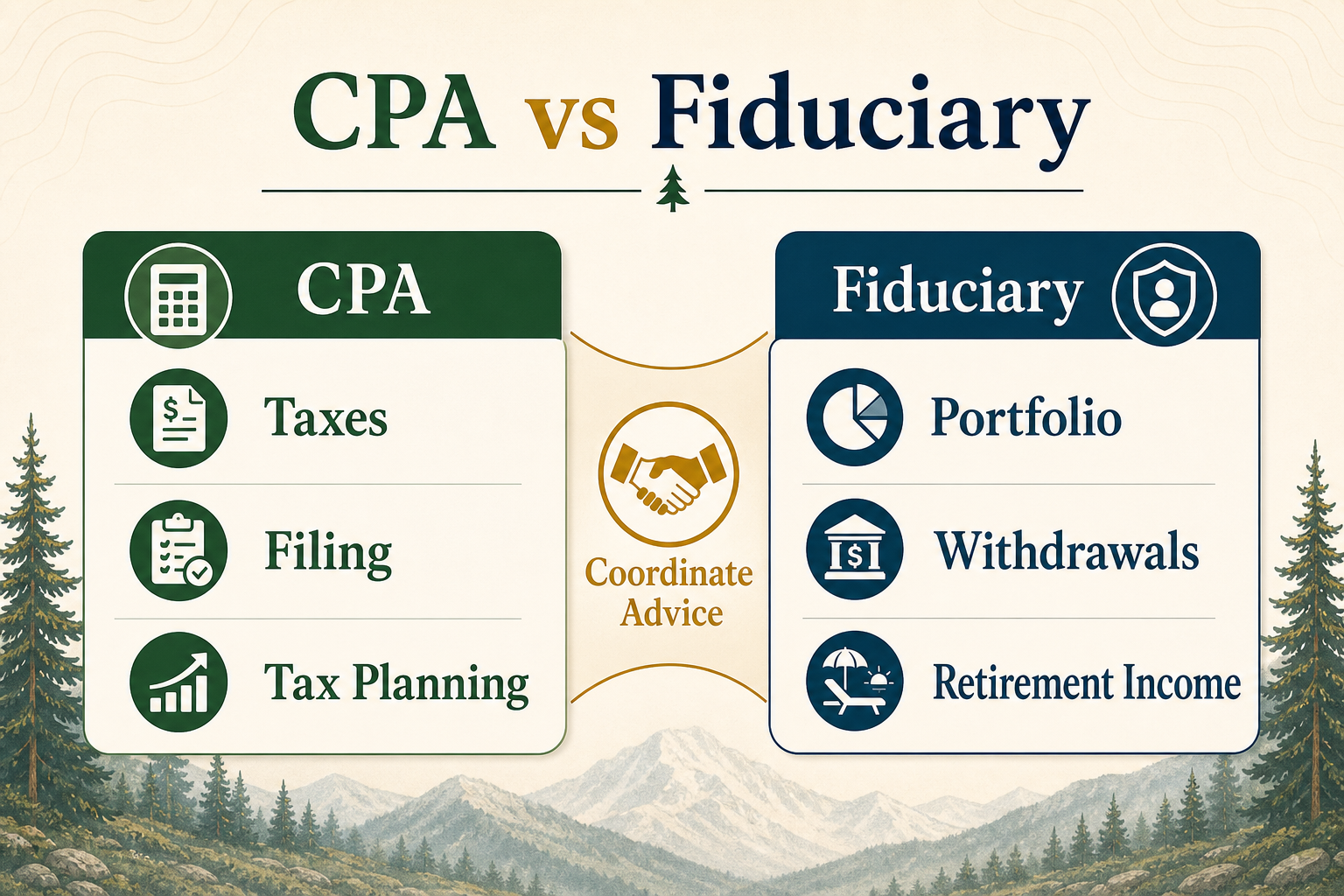

CPA vs fiduciary: who does what?

These roles overlap, but they are not identical.

When a CPA may be the right first call

A CPA is often the best first professional when the problem is mostly about taxes, tax planning, or high-impact reporting decisions. AICPA notes that its CPA/PFS path is built around tax expertise plus broader financial planning knowledge, which is why many households lean on a CPA when retirement, investments, estate planning, and taxes all interact.

You should seriously consider sitting down with a CPA once you have around $100,000 or more in liquid assets, especially if those assets create taxable decisions or if retirement planning is beginning to affect tax strategy.

When a fiduciary financial professional may be worth it

A fiduciary financial professional is about advice quality and duty, not just a job title. CFP Board states that when a CFP professional is providing financial advice to a client, that CFP professional must act as a fiduciary and therefore act in the client’s best interests. Investor.gov also stresses the importance of checking whether an investment professional is properly licensed and registered before working with them.

As a practical rule of thumb, we recommend seriously considering a fiduciary relationship once you have around $500,000 or more in liquid assets. At that level, portfolio construction, withdrawal planning, tax drag, and sequence risk often matter enough that oversight can be worth the cost.

These thresholds are not legal rules or universal planning standards. They are LEOFF Helper judgment calls meant to help people decide when professional help becomes worth considering.

LEOFF Helper is not recommending any specific CPA, fiduciary, advisory firm, or financial service. The point is only that some households should consider seeking qualified professional help once the stakes, complexity, or asset level become large enough.

Our rule-of-thumb asset thresholds

Here is the short version:

- Below $100,000 in liquid assets: many households can still manage with a strong DIY process, especially if taxes and investments are simple.

- Around $100,000+ in liquid assets: it is probably worth at least one conversation with a CPA, especially if taxes, retirement timing, or account strategy are becoming more important.

- Around $500,000+ in liquid assets: it becomes increasingly reasonable to consider a fiduciary financial professional, especially if retirement is approaching.

That does not mean a household under those numbers should never hire help, or that a household above them must hire help. It means the math starts to justify the conversation.

It also does not mean you should ignore your finances until you hit a large number like $1 million. In many cases, the opposite is true. If you build a good system early using accounts such as a 401(k), IRA, HSA, Roth accounts, 529 plans, and taxable savings in a tax-aware way, then by the time you reach a large portfolio you may already be in much better shape.

That is very different from someone who saves diligently but without a real structure and later arrives at retirement with a large, low-basis taxable portfolio or an inefficient account mix that is harder to unwind cleanly. The same dollar amount can create very different planning problems depending on how it was built.

When complexity matters more than the number

Regardless of the exact liquid-asset total, you should strongly consider a fiduciary financial professional if any of the following are true:

- Life becomes complex. You are dealing with inheritance, business exits, equity compensation, major tax issues, or concentrated positions.

- You lack time or expertise. You are too busy to manage your finances well, or you feel overwhelmed by investment and withdrawal decisions.

- The decisions are high-stakes. You are approaching retirement, or a 10% mistake on the portfolio would have major consequences for your plan.

This is the part many people miss. You do not need to wait until you are wealthy by someone else’s definition. Complexity can justify help earlier than asset size alone would suggest.

And the opposite can also be true: a household that has implemented a strong savings and account-location strategy early may need less corrective help later because the foundation is already sound. Even then, retirement itself can still be the point where professional advice becomes more valuable, because the challenge shifts from saving efficiently to drawing income efficiently.

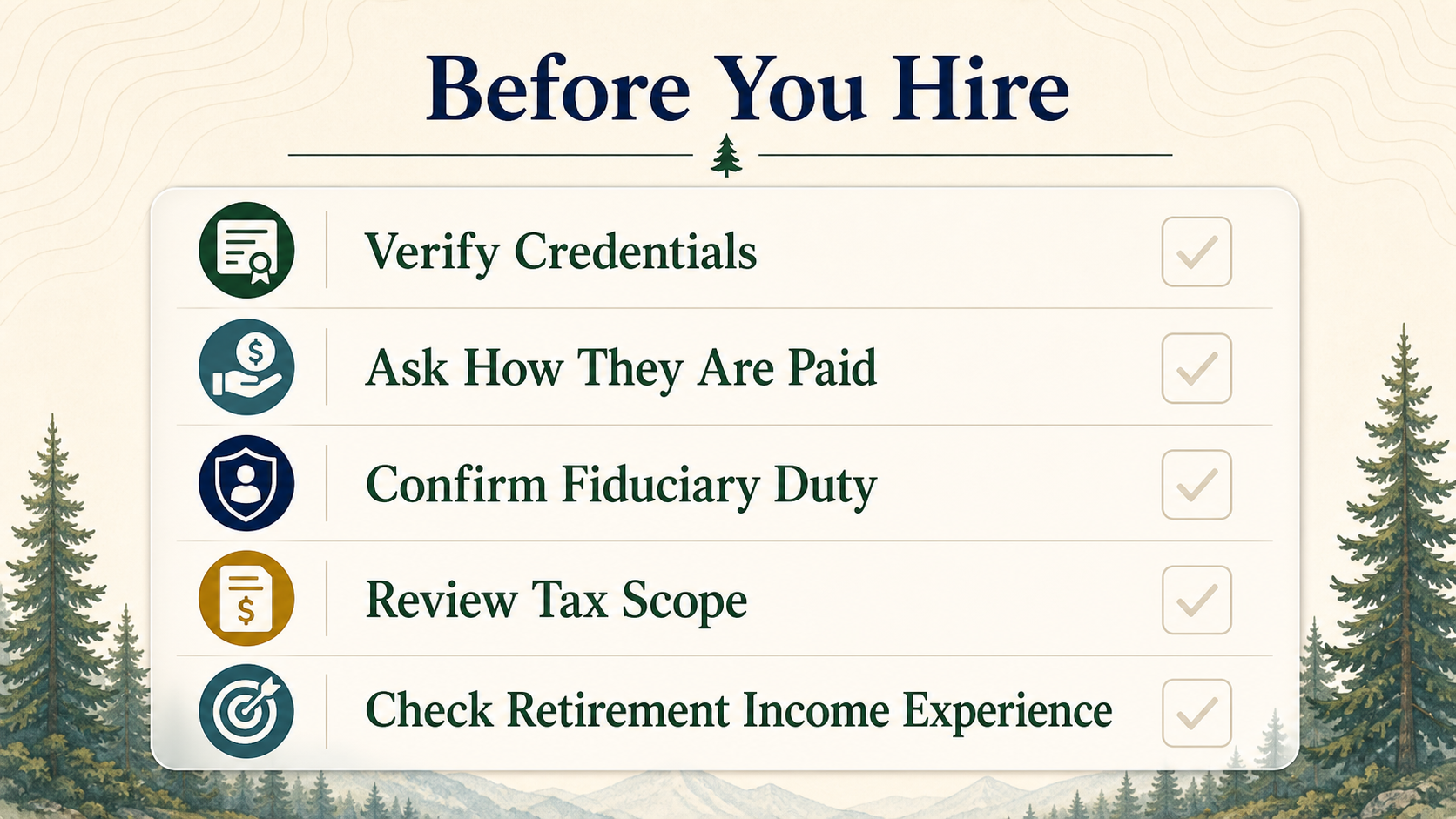

How to vet the professional you hire

Before hiring anyone, slow down and check the basics:

- Verify the person is licensed or registered where appropriate.

- Ask how they are paid.

- Ask whether they act as a fiduciary when giving advice.

- Ask whether tax planning is included or if you still need a separate CPA.

- Ask how they handle retirement-income planning, not just accumulation investing.

That still does not mean you must hire someone, and it does not mean LEOFF Helper is steering you toward a particular professional. It simply means this is the stage where outside expertise may be worth evaluating.

Investor.gov says retail investors should review the professional’s background and Form CRS when applicable. The IRS also notes that CPAs, attorneys, and enrolled agents have unlimited representation rights before the IRS, which can matter if your tax situation becomes more serious than routine preparation.

If you are mostly facing tax complexity, a CPA or CPA/PFS may be the right anchor relationship. If you are mostly facing investment, withdrawal, and retirement-allocation decisions, a fiduciary financial professional may be the better first hire. Many households eventually need both.

Model Your Plan FirstSources

CFP fiduciary duty and standards: CFP Code of Ethics and Standards of Conduct

CFP fiduciary-duty FAQ: Frequently Asked Questions about Duties Owed to Clients

Investor.gov guidance on checking investment professionals: Investment Professionals and Check Out Your Investment Professional

AICPA guidance on the CPA/PFS credential: Personal Financial Specialist (PFS) credential

IRS guidance on preparer credentials and representation rights: Understanding tax return preparer credentials and qualifications